Second the manufacturing overhead account tracks overhead costs applied to jobs. In this case the manufacturing overhead is overapplied by 500 10000 9500 as the applied overhead cost is 500 more than the actual overhead cost that have occurred during the period.

Assigning Manufacturing Overhead To Jobs Youtube

They consist of indirect materials indirect labor and miscellaneous expenses.

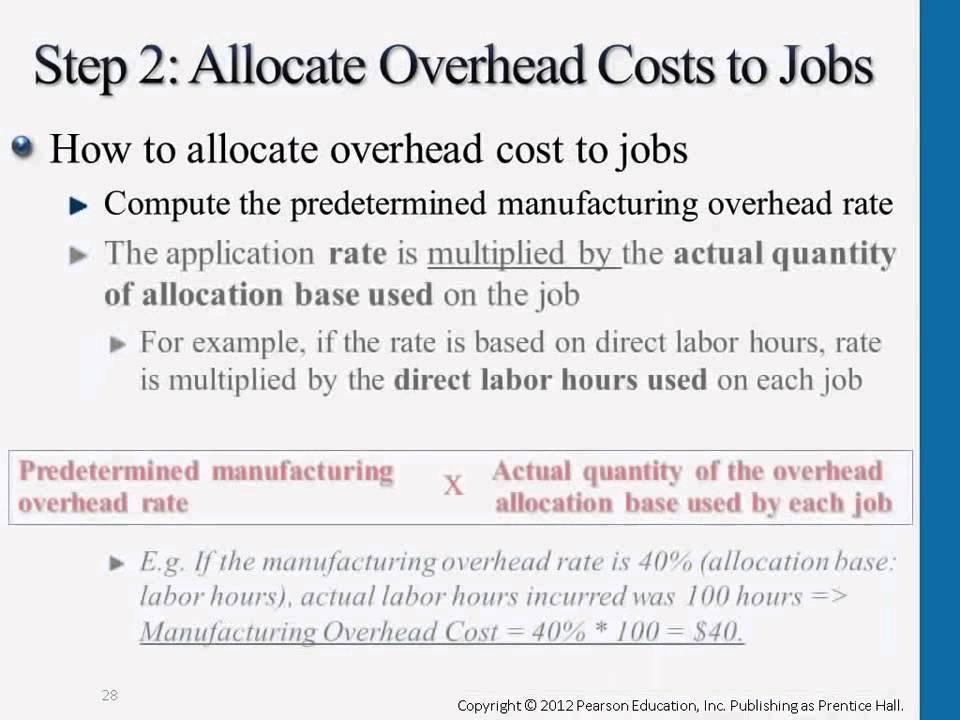

. Overhead applied to a particular job Predetermined overhead rate Amount of allocation incurred by the job. When this journal entry is recorded we also record overhead applied on the appropriate job cost sheet just as we did with direct materials and direct labor. The journal entry to reflect this is as follows.

If the company incurred 584300 in actual overhead costs and applied 585600 to jobs during the year was the overhead over- or under-applied for the year and if so by how much. Answer --The statement is FALSE. The manufacturing overhead cost would be applied to this job as follows.

During the same period the Manufacturing Overhead applied to Work in Process was 75000. Occurs when actual overhead costs debits are lower than overhead applied to jobs credits. We review their content and use your feedback to keep the quality high.

The journal entry to apply manufacturing overhead costs to completed jobs credits either Applied Manufacturing Overhead or Manufacturing Overhead Control True O O False. Here overhead is estimated to include indirect materials 50 worth of coffee indirect labor 150 worth of maintenance and other product. The manufacturing overhead cost assigned to the job is recorded on the job cost sheet of that particular job.

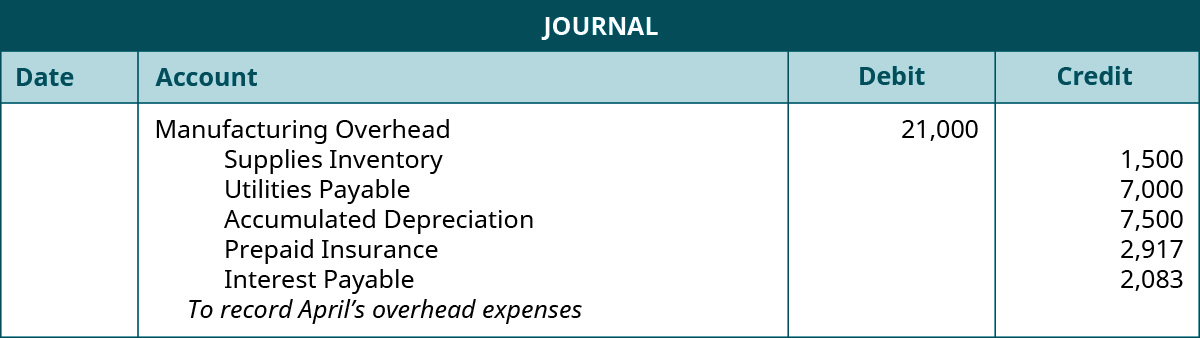

The entry to record these expenses increases the amount of overhead in the manufacturing overhead account. The journal entry to apply manufacturing overhead costs to completed jobs credits either Applied Manufacturing Overhead or Manufacturing Overhead Control. Overhead applied Pre-determined overhead rate X.

If the job in work in process has recorded actual material costs of 4640 for the accounting period then the predetermined overhead applied to the job is calculated as follows. Overhead expenses are all costs on the income statement except for direct labor direct materials and direct expenses. Overhead applied to job 2B47 Predetermined.

Overhead applied to a particular job Predetermined overhead rate Amount of the allocation base incurred by the job 800 27 DLH 216. However the manufacturing overhead costs that it has applied to the production based on the predetermined standard rate is 10000 for the period. Note that the job cost sheet in the example below indicates that 27 labor hours have been worked.

Prepare a journal entry to close out balance of under applied overhead to cost of goods sold. The process of determining the manufacturing overhead calculation rate was explained and demonstrated in Accounting for Manufacturing Overhead. Stickles Corporation incurred 79000 of actual Manufacturing Overhead costs during August.

The over or under-applied manufacturing overhead is defined as the difference between manufacturing overhead cost applied to work in process and manufacturing overhead cost actually incurred by the entity during the period. In the journal entry to close overapplied overhead Cost of Goods Sold is credited. Applied overhead Predetermined overhead rate x Actual activity base units Applied overhead 03125 x 4640 1450.

Recording the application of overhead costs to a job is further illustrated in the T-accounts that follow. The journal entry to reflect this is as follows. The overhead costs applied to jobs using a predetermined overhead rate are recorded as credits in the manufacturing overhead account.

During the year manufacturing overhead is applied to jobs in work-in-process using the following formula. See the following calculation. At the end of the accounting period manufacturing overhead costs are applied to uncompleted jobs using the same.

View the full answer. Because manufacturing overhead is applied at a rate of 30 per direct labor hour 180 30 6 hours in overhead is applied to job 50. Debit to Manufacturing Overhead of 79000.

Recording the application of overhead costs to a job is further illustrated in the T-accounts that follow. The journal entry to record the incurrence of the actual Manufacturing Overhead costs would include a. To do this simply take the monthly manufacturing overhead and divide it by monthly sales then multiply the total by 100.

If your manufacturing overhead rate is low it means that the business is using its resources efficiently and effectively. The amount of overhead applied to Job MAC001 is 165. If the manufacturing overhead cost applied to work in process is more than the.

Therefore a total of 216 of manufacturing overhead cost would be applied to the job. The actual manufacturing overhead incurred during January was 26000. During January job numbers A79 and N08 were completed and job number A79 was sold.

Costs such as direct materials and labor are calculated in the cost of goods sold and indirect costs. The estimated manufacturing overhead cost applied. Although calculating overhead varies depending on the method used there are three general types of expenses for manufacturing businesses.

Once you have calculated your indirect costs you must complete another calculation your manufacturing overhead rate. The overhead costs applied to jobs using a predetermined overhead rate are recorded as credits in the manufacturing overhead account. Manufacturing Overhead Rate Overhead Costs Sales x 100 Manufacturing Overhead Rate 80000500000 x 100 This means 16 of your monthly revenue will go toward your companys overhead costs.

Over-applied 585600 584300 1300 APPLIED GREATER THAN Actual. Because manufacturing overhead is applied at a rate of 30 per direct labor hour 180 30 6 hours in overhead is applied to job 50. 110000 charged to specific jobs and.

The next journal entry shows the reduction of cost of goods sold to offset the amount of overapplied overhead. In this last example 100000 was actually spent and accounted for. The journal entry to apply manufacturing overhead costs to completed.

Overhead expenses include accounting fees advertising insurance interest legal fees labor burden rent repairs supplies taxes telephone bills travel expenditures and utilities. Rashid Javed Updated on. Always keep in mind that the goal is to zero out the Factory Overhead account and measure the actual cost incurred.

Prepare Journal Entries For A Job Order Cost System Principles Of Accounting Volume 2 Managerial Accounting

Assigning Manufacturing Overhead Costs To Jobs Accounting For Managers

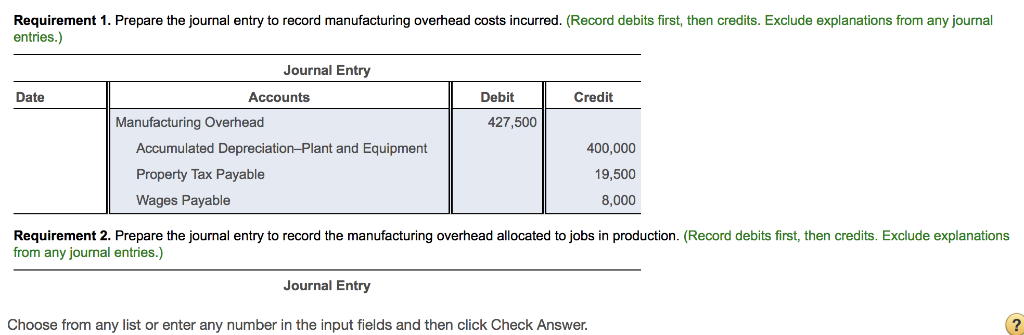

Solved Requirement 1 Prepare The Journal Entry To Record Chegg Com

Assigning Manufacturing Overhead Costs To Jobs Accounting For Managers

0 Comments